The ASE Fleet's Weekly Take Off 22

The ASE Fleet's Weekly Take Off 22

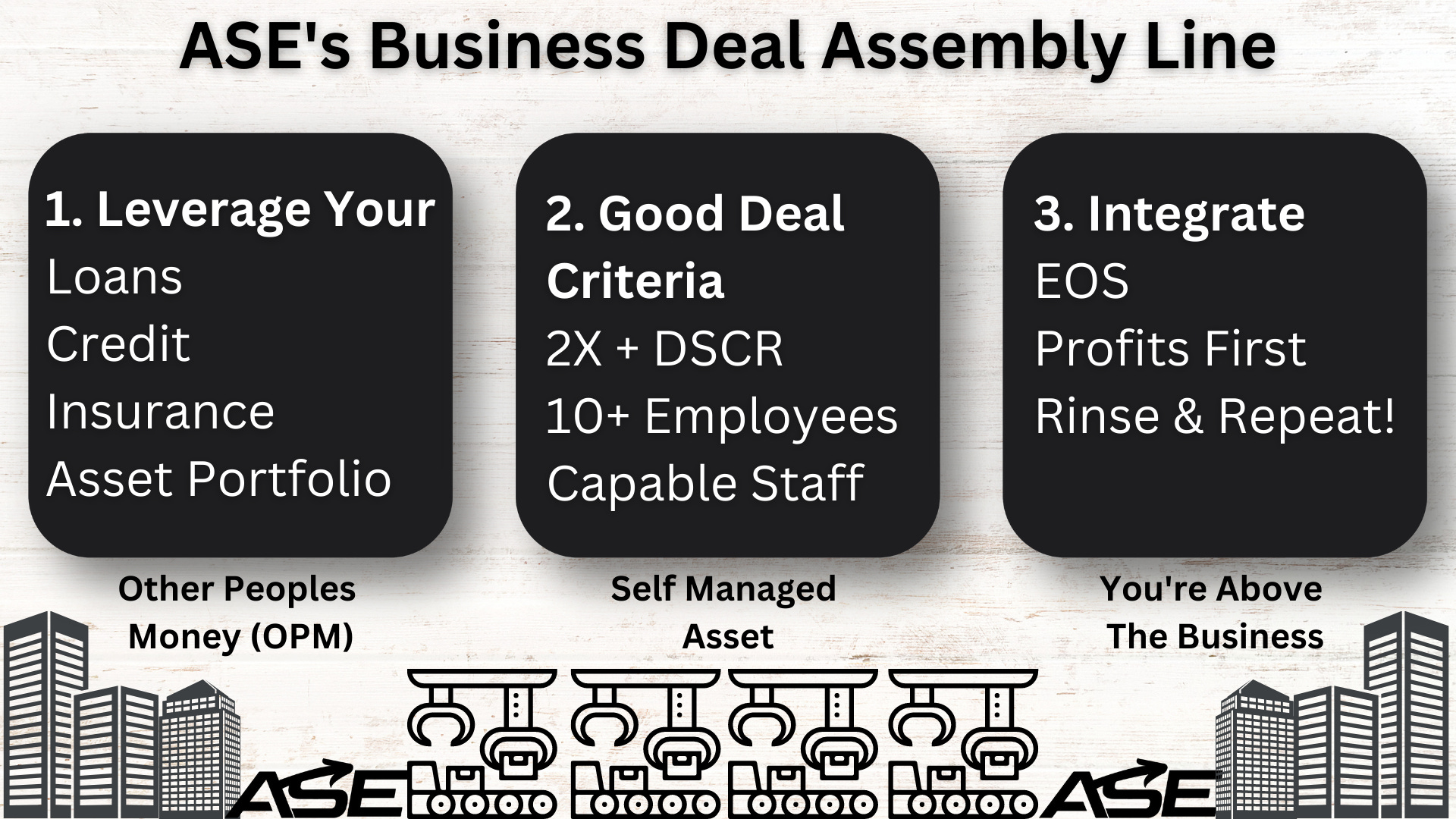

The Valuation Phase Of The M&A Lifecycle

Hello Freinds!

If you haven’t seen or heard, the market tanked to 3x multiples, and for deals under a $5M ask, calculating valuations with EBITDA and not net profit is for the birds.

And this short post will keep you from overpaying on your next deal.

In mergers and acquisitions (M&A), the valuing of companies is conducted so that the buyer knows how much money they are willing to spend. And so that the seller knows that they’re getting a fair valuation of their business.

The Valuation Phase evaluates the financials and overlapping expenses that can be consolidated like insurance, utilities, services, and software subscriptions. Beyond the financials, anticipated synergies like culture fit, operations, and the addressable market/client profile.

In this post, we’ll talk about what you need to know about the Valuation Phase and give you some tips to help you reach a win-win deal on both the sell and buy-side.

What is a Business Valuation?

A business valuation is the process of determining the current worth of a business.

Just like with real estate, the market value of a company will fluctuate according to current economic variables.

The buyer or seller has to find the industry’s average EBTIDA multiple to value a company.

Second, the buyer must evaluate the target company’s financials to see if the company can support debt or determine how long it will take to get a return on investment (ROI).

Third, estimate and map out the anticipated synergies from this transaction, which can make it more valuable.

Note: For the sell-side, you need to make sure that you complete our 8 Steps for Selling Your Business Checklist at least 1 year before you plan to sell.

The Financial Analysis

The financial analysis is the first step to evaluating a company for an acquisition. This analysis will include the company’s balance sheet, income statement, cash flow statement, and the market value of the company’s stock (when applicable).

A multiple of EBITDA will usually be used to value the company. And I know that Warren Buffet thinks it’s a joke, but it’s also become the standard method of communicating a company’s value.

The formula for EBITDA is:

EBITDA = E + I + T + D + A

EBITDA = Earnings Before Interest, Taxes, Depreciation, and Amortization

E = net income

I = interest

T = taxes

D = depreciation

A = Amortization

Suppose your company is doing less than $2M in topline/revenue. In that case, a multiple of EBIT may be used. EBIT is the same as EBITDA but without depreciation or amortization.

The second half involves getting the business’s valuation multiple by industry, which you can get from the business brokerage press or the NYU Stern School of Business’s website.

You can usually expect a 2-4x multiple for lower-market deals under $2M based on how organized the selling company is.

The Evaluation of Anticipated Synergies

What does an anticipated synergy mean? It’s the expected savings and gains from the merger or acquisition. These savings can come from reduced operating costs, such as lower marketing expenses, carve-outs (selling off excess or duplicate assets), utilities, insurance, outsourced services, and other subscriptions.

Gains will usually come in the form of cross-pollinating business and leveraging both sides’ management, assets, Intellectual Property like systems, customer lists, testimonials and clout, and sales and marketing.

The best way to estimate synergies is to think about how the transaction will make the combined company more efficient and put a Strength, Weakness, Opportunity, and Threat (SWOT) Analysis of each company side by side.

Then start asking questions like:

How can each company benefit from the combined resources?

Is there any overlap in the employee’s skillsets?

If yes, is one better, or are they both rock stars?

What are the primary skill sets of each company?

How can the combined company leverage these skillsets?

Would it be best to keep each company standing on its own two feet?

The answers to these questions will give you a good idea of how much of a synergy you’re likely to see after the merger or acquisition.

The difference between a merger and an acquisition is that both companies become 1 as 50/50 (or whatever ratio is negotiated) partners in a merger. On the other hand, in an acquisition, one company holds 100% ownership and takes over the other company’s assets.

How to Negotiate the Best Price for Your Company

When you sell your company to a buyer, they are going to want to know what you think your company is worth. And as a seller, it’s important to understand what you want in return for your company.

If you know what you want to get out of your transaction, then you can negotiate for it. If you plan to buy a house, car, watch, or any other asset with the sale of your business, let them know that too.

You can also use data that the buyer has disclosed about themselves to help negotiate the best price based on the current market value.

Staying within your market’s multiple will guarantee that your company sells. Which may be difficult because of the emotional attachment to your company or because you’re trying to build wealth off one single transaction.

These psychological fallacies are why 90% of the companies that hit the market never sell.

Right next to business brokers, convincing the seller that their business is worth the highest possible multiple per their real estate training.

That’s why a few thousand strategic buyers in the ASE consortium and in the M&A space, in general, won’t touch broker deals with a barge pole.

Nothing against the brokers; that’s just the side effect of relying on real estate training and methods in a business environment that has more moving parts.

If you need help valuing your company, ASE’s business valuation services are only $3,000.00.

If you’re still deciding whether or not to sell your company subscribe to our newsletter to take the Above the Business Score.

That way, if you decide to sell, you can get more cash in your pocket, and if you decide not to sell, you’ll have more take-home (net profit) by leveraging your score’s results and our operating systems.

Source:

https://www.acquirescaleandexit.com/what-is-the-mergers-and-acquisitions-ma-valuation-phase/

Meme Of The Week

Darn! Well, it looks like the cat's out of the bag now.

Post Of The Week

How To Be Your Own Personal Investment Bank

Real estate investors have been making their money multi-task like a single mom for decades!

And when we discovered infinite banking, we went berserk!

Because getting the 10% - 20% down payment for a loan is one of the biggest headaches for M&A, real estate, and all other entrepreneurs.

Infinite banking is the most exciting tool for deal makers, and we can share how our team members are setting themselves up to be their own personal M&A bank.

In a nutshell, if you're putting $200k down for a mortgage/loan/investment, we can put that capital into a whole life insurance policy for you, and then you can loan yourself that same $200k from the policy.

But when they pay the policy loan back, you have access to that $200k again for the next deal, while the original $200k in the policy grows via interest.

Yes, your money is working overtime for you now!

You can only borrow the cash value that's in the policy, so it's also a great way of saving for large purchases and retirement. And one of our senior advisors specializes in funding whole-life policies without decreasing your lifestyle.

Our team must conduct a full financial diagnosis before recommending anything, as there are other factors like protecting your health, family, and retirement.

So ASE invites you to meet our team over a phone or video call.

And if you’re in Denver, we can meet in person:

2000 South Colorado Blvd. Denver, Colorado 80222

MassMutual is the #1 finance firm in the country, and we pay a generous referral bonus for anyone that you recommend to our team.

Deals Of The Week

Here are all of our off-market companies for sale and a list of vetted business buyers:

https://docs.google.com/document/d/1wU2ZctV_KZnNDPpS_NNpLNp2nhNMLxOn5YbVZIwlyQU/edit?usp=sharing

Best viewed on PC for a clickable table of contents on the left.

And bookmark the link. It's a live Rolodex!

*Disclaimer these deals are usually a better fit for a strategic buyer; because great deals don't last very long on here. At the same time, since it's not a public site, there isn't as much competition as public sites. So you ought to check the deal sheet weekly. Reach out to us for the NDA and full CIM on any of these deals*

Financial Architecting Tip Of The Week

The ASE Fleet's Financial Architecting Tool #10

Accredited Investors

Private capital always moves faster than institutional capital!

"An accredited investor is an individual or a business entity that is allowed to trade securities that may not be registered with financial authorities. They are entitled to this privileged access by satisfying at least one requirement regarding their income, net worth, asset size, governance status, or professional experience.

In the U.S., the term accredited investor is used by the Securities and Exchange Commission (SEC) under Regulation D to refer to investors who are financially sophisticated and have a reduced need for the protection provided by regulatory disclosure filings. Accredited investors include high-net-worth individuals (HNWIs), banks, insurance companies, brokers, and trusts."

Source: Investopedia

https://www.investopedia.com/terms/a/accreditedinvestor.asp

Deal Trophy Of The Week

Business Buyer Of The Week

We work with over 20 of the most active buyers in the United States across every industry as M&A advisors.

Click here for our criteria:

https://docs.google.com/spreadsheets/d/1oGisPRVIa2TsG4n_G8oNOrlLh2PoxiSObtJlRZISv7s/edit?usp=sharing

This buyer has a $2.3B budget:

The 11th Issue of Acquisition Aficionado Magazine is now LIVE!

Act NOW to avoid missing out!

Visit the website to download your free copy now while you still can -

This month, you'll hear the latest success stories and advice from

leading figures in the business acquisition industry, just take a sneak

peek at what's in store for you by reading this month's copy:

*The Power of Roll-Ups - Carl Allen

*Why List Price Multiples Don't Matter as Much as You Think - Joe

Valley, Quiet Light Brokerage

*The Basics of a Business Purchase Agreement - Live Oak Bank

*5 Hard Lessons Learned from 48 Pandemic Acquisitions - Jonathan Jay

*4 Things You Didn't Know About M&A Insurance - AcquireCover Insurance

*10 Practices for Acquired Employee Onboarding in M&A - Chris von

Bogdandy

*5 Reasons to Consider Selling Your Business to a Search Fund - The

Hatchit Marketplace

*Three Key Considerations for Maximizing Value for a Small to

Medium-Sized Business - Koji Bratcher

*How2Exit Episode 60: Tim Mueller & Ron Skelton

*Value Creation: The Holy Grail of M&A - Adrian Knight, Managing Partner

at Knight Equity

* How to Close Deals in a Recession - Edgar Fernandez of Acquire Scale

and Exit

Act NOW to avoid missing out!

Visit the website to download your free copy now while you still can -